Financial review

Overview

Dairy Crest has continued to make progress in difficult trading conditions and 2014/15 saw an important step in delivering against our long term strategy.

In November 2014 we announced that we had agreed to sell our Dairies operations to Müller. The sale has been approved by shareholders but remains subject to the approval of the CMA. Completion of this sale will deliver a step-change in delivering our strategy of creating a value-added, streamlined business with reduced exposure to commoditised markets and the ability to deliver future growth both organically and through acquisitions.

Overall, the financial performance of the Group during the year has been satisfactory. The performance of the operations we expect to retain, namely Cheese and whey and Spreads and butter (“the Retained business”) has been strong with revenue and product group profits up 0.5% and 19.3% respectively and a fully costed margin of 15%. However, profits in our Dairies operations have reduced markedly in the year reflecting strong competition in liquid milk markets and sharp falls in commodity realisations.

We have continued to invest in the businesses we are retaining. Our investment at our spreads site at Kirkby enabled us to close Crudgington during the year and the new demineralised whey and galacto-oligosaccharide facilities at Davidstow, which are nearing completion, will increase future whey returns. Having completed these investments, the businesses to be retained will run out of five well-invested, efficient processing sites.

Sale of Dairies operations

The sale of our Dairies operations to Müller remains on track and, subject to clearance by the CMA, is expected to complete during the year ending 31 March 2016.

The sale includes the FRijj brand and bulk butter manufacture and the Dairies supporting overhead structure to Müller for £80 million, payable in cash, on completion. This includes the factories at Foston, Chadwell Heath and Severnside. It also includes the Hanworth glass bottling site, where Dairy Crest has consulted with employees on the site’s future, and the depot distribution network.

Dairy Crest will retain full ownership of the closed dairies at Totnes and Fenstanton, its Chard site and a number of previously closed depots and will sell these in the future.

Under the terms of the sale agreement the two companies will also enter into a supply agreement whereby Müller will sell bulk butter to Dairy Crest for five years. In addition Dairy Crest will provide certain transitional IT services to Müller.

Dairy Crest will continue to be responsible for the defined benefit pension obligations in relation to the closed Dairy Crest Group Pension Fund.

Any consideration payable by Müller is subject to upward or downward adjustments for variances from agreed levels of working capital, capital expenditure and the profitability of Dairy Crest’s Dairies operations and will also be adjusted to reflect profits made on the sale of properties included in the transaction that are sold by Dairy Crest before completion.

Müller has the ability not to complete their purchase of our Dairies operations should there be a material deterioration of more than £20 million in the agreed level of profitability of Dairy Crest’s Dairies operations before completion. At this time we do not anticipate that there will be such a material deterioration in the profitability of our Dairies operations before completion. Müller may also not complete if any of our four dairies are inoperable when completion is due.

The sale constitutes a Class 1 transaction for Dairy Crest pursuant to the Listing Rules. Shareholder approval was received on 23 December 2014.

Following shareholder approval for the sale, we are separating our Dairies operations, including the relevant IT systems, from the rest of the business. This creation of a stand-alone Dairies operation is necessary for completion of the sale but also ensures that supporting overhead costs are fully transferred along with the underlying business. Furthermore, it results in both the retained business and the Dairies business staying focussed on delivering their plans until such time as the sale completes.

Because the sale remains conditional upon approval from the CMA it was not, at 31 March 2015, considered to have met the “highly probable” criteria required under IFRS 5 in order for the Dairies business to be classified as held for sale. This judgement will be kept under review as the CMA continues its review of the transaction.

We continue to provide product group analysis consistent with prior years to assist the users of the Financial Statements although the Group operated as one segment throughout 2014/15.

|

Product group revenue |

2015 £m |

2014 £m |

Change £m |

Change |

|

Cheese and whey |

274.4 |

264.6 |

9.8 |

3.7% |

|

Spreads and butter |

170.0 |

177.4 |

(7.4) |

(4.2%) |

|

Other |

3.8 |

4.2 |

(0.4) |

(9.5%) |

|

Retained business |

448.2 |

446.2 |

2.0 |

0.4% |

|

Dairies |

881.6 |

944.8 |

(63.2) |

(6.7%) |

|

Total external revenue |

1,329.8 |

1,391.0 |

(61.2) |

(4.4%) |

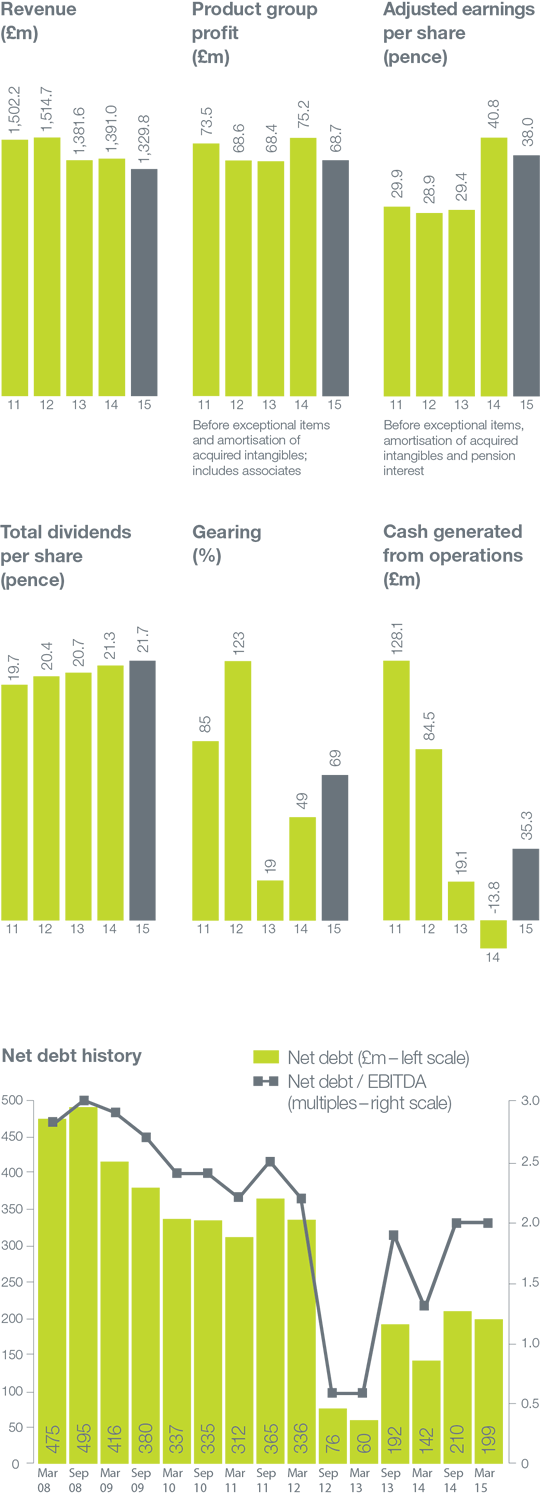

Revenues from our Retained business increased marginally which represents a good performance in categories experiencing price deflation. In particular, Cathedral City has had another strong year with revenue up by 5%. Conversely, our Dairies operations have seen some volume declines along with significant price deflation and overall revenue has reduced by 6.7% in the year to £881.6 million.

|

Product group profit |

2015 £m |

2014 £m |

Change £m |

Change |

|---|---|---|---|---|

|

Cheese and whey |

33.1 |

39.3 |

(6.2) |

(15.8%) |

|

Spreads and butter |

33.8 |

16.8 |

17.0 |

101.2% |

|

Retained business |

66.9 |

56.1 |

10.8 |

19.3% |

|

Share of associate |

– |

0.3 |

(0.3) |

n/a |

|

Dairies |

1.8 |

18.8 |

(17.0) |

(90.4%) |

|

Total product group profit |

68.7 |

75.2 |

(6.5) |

(8.6%) |

|

Remove share of associate |

– |

(0.3) |

0.3 |

n/a |

|

Acquired intangible amortisation |

(0.4) |

(0.4) |

– |

– |

|

Group profit on operations (pre-exceptional items) |

68.3 |

74.5 |

(6.2) |

(8.3%) |

Overall Group product group profit (before interest, acquired intangible amortisation and exceptional items) fell by 8.6% to £68.7 million. However, product group profit of the businesses we are retaining grew by 19.3% to £66.9 million.

Cheese and whey profits reduced somewhat after a very strong year ended 31 March 2014 as the cost of sales reflected milk cost increases in that year and whey realisations softened in the second half of the year ended 31 March 2015. Lower milk input costs during the year ended 31 March 2015 have resulted in the cost of cheese in stock falling. However, due to the maturity profile of cheese, this will not be fully reflected in reduced cost of goods sold until the second half of the year ending 31 March 2016.

Spreads and butter profits were higher following a difficult 2013/14 principally as a result of significantly lower cream input costs.

Overall margins in the retained businesses increased from 13% in 2013/14 to 15% in 2014/15. These margins are stated after allocating all costs including central administrative overheads of the Group.

Dairies profits fell despite lower milk input costs, reflecting the competitive marketplace and significantly lower dairy commodity realisations. Within this, profits from the sale of closed depots were marginally lower at £17.6 million (2014: £18.2 million). The Dairies business stabilised somewhat in the second half of the year and losses (before property profits) reduced from £11.9 million in the first half to £3.9 million in the second half. However, the dairy sector remains challenging and contract renewals and continued weak commodity returns will continue to put pressure on our Dairies operations in 2015. Although we retained our contract to supply Morrisons for a further three years following a competitive tender, the volumes we expect Morrisons to purchase have reduced by around one third from March 2015.

Exceptional items

Pre–tax exceptional charges in the year totalled £36.3 million (2014: £10.4 million). Cash exceptional operating costs reduced to £19.8 million (2014: £20.8 million).

Exceptional charges of £16.7 million were associated with the final consolidation of Spreads and butter production at Kirkby along with the installation of a bulk butter churn at Severnside and the creation of a new innovation centre at Harper Adams University. The Crudgington site was closed in December 2014 and any further exceptional costs associated with the completion of the Innovation Centre will be more than offset by future exceptional profit from the sale of the Crudgington production site.

Exceptional costs of £3.4 million relate to the investment in demineralised whey and galacto-oligosaccharide. These relate predominantly to incremental site costs incurred as a result of the significant works being undertaken, for example additional site shut downs. These projects remain on track for completion later in 2015.

In September 2014 we announced the future closures of our glass bottling site at Hanworth and our specialist cream potting facility at Chard. £11.8 million of exceptional charges have been made in respect of these closures of which £9.2 million are non-cash asset write downs and accelerated depreciation.

Further exceptional costs of £4.3 million have been charged in respect of the proposed sale of our Dairies operations. These include costs associated with the transaction, predominantly professional fees as well as costs relating to the separation of the Dairies business into a standalone entity.

Finance costs

Finance costs of £8.1 million reduced by £2 million in the year reflecting some capitalised interest on the major projects at Kirkby and Davidstow as well as the repayment of £27 million of loan notes in April 2014 that were at effective fixed rates of 4.97%. Interest cover excluding pension interest, calculated on total product group profit increased to 8.5 times (2014: 7.6 times).

Other finance expenses, which are derived by applying the discount rate to pension scheme assets and liabilities at the start of each financial year, increased to £1.8 million (2014: £0.3 million). These amounts are dependent upon the pension scheme position at 31 March each year and are volatile, being subject to market fluctuations. We therefore exclude this item from headline adjusted profit before tax.

|

Profit before tax |

2015 £m |

2014 £m |

Change £m |

Change |

|---|---|---|---|---|

|

Total product group profit |

68.7 |

75.2 |

(6.5) |

(8.6%) |

|

Finance costs |

(8.1) |

(9.9) |

(1.8) |

(18.2%) |

|

Adjusted profit before tax |

60.6 |

65.3 |

(4.7) |

(7.2%) |

|

Amortisation of acquired intangibles |

(0.4) |

(0.4) |

– |

|

|

Exceptional items |

(36.3) |

(10.4) |

(25.9) |

|

|

Other finance expense – pensions |

(1.8) |

(0.3) |

(1.5) |

|

|

Reported profit before tax |

22.1 |

54.2 |

(32.1) |

(59.2%) |

Adjusted profit before tax (before exceptional items and amortisation of acquired intangibles) decreased by 7% to £60.6 million. This is managements’ key Group profit measure. Reported profit before tax of £22.1 million represents a £32.1 million decrease from 2014 predominantly due to the higher level of exceptional items incurred in 2015.

Taxation

The Group’s effective tax rate on continuing operations fell slightly to 14.0% (2014: 14.6%). The effective tax rate continues to be below the headline rate of UK corporation tax due to property profits on which tax charges are offset by brought forward capital losses or roll-over relief.

Group profit for the year

The reported Group profit for the year was £22.1 million (2014: £54.2 million).

Earnings per share

The Group’s adjusted basic earnings per share from continuing operations fell by 6.9% to 38.0 pence (2014: 40.8 pence). Basic earnings per share from continuing operations, which includes the impact of exceptional items, pension interest expense and the amortisation of acquired intangibles, amounted to 15.0 pence (2014: 35.8 pence).

Dividends

We remain committed to a progressive dividend policy and have continued to deliver against that policy by increasing our proposed dividend. The proposed final dividend of 15.7 pence per share represents an increase of 0.3 pence per share – a 1.9% increase. Together with the interim dividend of 6.0 pence per share (2014: 5.9 pence per share) the total proposed dividend is 21.7 pence per share (2014: 21.3 pence per share). The final dividend will be paid on 6 August 2015 to shareholders on the register on 3 July 2015.

Dividend cover of 1.8 times is within the target range of 1.5 to 2.5 times (2014: 1.9 times).

Pensions

The latest full actuarial valuation of the closed defined benefit pension scheme was performed at 31 March 2013 and resulted in an actuarial deficit of £105 million taking into account the one-off contribution of £40 million we made to the scheme in April 2013.

During the year ended 31 March 2015 the Group paid £13 million cash contributions into the scheme in line with the new schedule of contributions agreed with the Trustee in March 2014. This level of contributions will continue for the year ending 31 March 2016 before increasing to £16 million for the year ending 31 March 2017.

During the year the focus of the Trustee and the Group has been to reduce the scheme’s exposure to equities in line with the derisking flight path agreed as part of the 2013 actuarial review. The proportion of assets (excluding insurance) held in higher risk/ higher return type assets has reduced from 75% at March 2014 to 61% at March 2015.

The reported deficit under IAS 19 at 31 March 2015 was £41.4 million a decrease of £16.3 million from March 2014. Asset returns have been strong during the year and have offset a further reduction in the discount rate used to measure liabilities. We continue to stick to a derisking programme that targets a self-sufficient scheme by 2019 requiring returns at that point of only 0.5% above gilt yields.

Cash flow

Our ambition is for the business to generate strong free cash flows in future years and we are making good progress towards this target. Pension contributions have reduced from levels seen in previous years and lower milk input costs have reduced the value of cheese stocks. Capital expenditure, which has been high for several years and peaked this year, will fall significantly following the completion of the demineralised whey and galacto-oligosaccharide projects in Davidstow in the first half of 2015/16. Furthermore, the sale of our Dairies operations will reduce exceptional restructuring costs in future years and result in one-off sales proceeds.

In the year ended 31 March 2015 cash generated by operations was £35.3 million (2014: £13.8 million outflow). This includes a working capital increase of £12.8 million albeit there has been a working capital reduction of £27.8 million in the second half of the year. Working capital changes reflect lower cost cheese stocks offset by the timing of customer receipts and supplier payments at the end of the year. Cheese stock valuations should continue to decrease in the year ending 31 March 2016 as higher cost cheese is sold and replaced in stock with that made at reduced milk input costs. Cash generated by operations also reflects reduced payments to the pension scheme as described above and exceptional cash costs of £19.8 million (2014: £20.8 million).

Cash interest payments amounted to £10.5 million (2014: £14.0 million). There were no net tax payments or receipts (2014: net receipt of £2.1 million).

Capital expenditure of £80.1 million (2014: £58.8 million) reflects the investments at Kirkby, Harper Adams and, in particular, at Davidstow, which together totalled £53.3 million as well as ongoing expenditure elsewhere in the business. In total capital expenditure was somewhat higher than we anticipated as we took the opportunity to accelerate investment in some other site infrastructure at Davidstow to avoid disruption in the future. We expect capital expenditure to fall below levels of depreciation once our investment in Davidstow is complete in summer 2015.

Proceeds from property disposals remain strong. In the year ended 31 March 2015 these totalled £21.1 million (2014: £25.1 million).

Net debt

Net debt includes the fixed Sterling equivalent of foreign currency loan notes subject to swaps and excludes unamortised facility fees.

Net debt increased from £142.2 million at 31 March 2014 to £198.7 million at 31 March 2015, somewhat higher than was anticipated due to the working capital movements and higher capital expenditure referred to above. However the ratio of net debt to EBITDA at 31 March 2015 remained within our target range of 1.0 to 2.0 times. Looking ahead, we expect net debt to fall by at least £20 million in the year ending 31 March 2016 mainly as a result of reduced capital expenditure.

At 31 March 2015, gearing (being the ratio of net debt to shareholders’ funds) was 69% (2014: 49%).

Borrowing facilities

The Group has £145 million loan notes outstanding which mature between 2016 and 2021 and a £170 million plus €90 million revolving credit facility expiring in October 2016. We expect to refinance our revolving credit facility in 2015.

Treasury Policies

The Group operates a centralised treasury function, which controls cash management and borrowings and the Group’s financial risks. The main treasury risks faced by the Group are liquidity, interest rates and foreign currency. The Group only uses derivatives to manage its foreign currency and interest rate risks arising from underlying business and financing activities. Transactions of a speculative nature are prohibited. The Group’s treasury activities are governed by policies approved and monitored by the Board.

Going concern

The financial statements have been prepared on a going concern basis as the Directors are satisfied that the Group has adequate financial resources to continue its operations for the foreseeable future. In making this statement, the Group’s Directors have: reviewed the Group budget, strategic plans and available facilities; have made such other enquiries as they considered appropriate; and have taken into account ‘Going Concern and Liquidity Risk: Guidance for Directors of UK Companies 2009’ published by the Financial Reporting Council in October 2009.

Tom Atherton Finance Director

20 May 2015