106

IMI plc

3.2.2 Goodwill impairment testing

Goodwill is not subject to an annual amortisation charge, instead, its carrying value is assessed annually by comparison to the future cash flows of the

business to which it relates (the cash generating unit, or CGU). These cash flows are discounted to reflect the time value of money and this discount rate,

together with the growth rates assumed in the cash flow forecasts, are the key assumptions in this impairment testing process.

Goodwill is allocated to cash generating units (‘CGUs’) based on the synergies

expected to be derived from the acquisition upon which the goodwill arose.

The Group has 24 cash generating units to which goodwill is allocated.

Where our businesses operate closely with each other we will continue

to review whether they should be treated as a single or combined CGU.

Goodwill is tested annually for impairment as part of the overall assessment of

assets against their recoverable amounts. The recoverable amount of a CGU is

the higher of its fair value less costs to sell and its value in use. Value in use is

determined using cash flow projections from financial budgets, forecasts and

plans approved by the Board covering a five-year period. The projected cash

flows reflect the latest expectation of demand for products and services.

The key assumptions in these calculations are the long-term growth rates and

the discount rates applied to forecast cash flows in addition to the achievement

of the forecasts themselves. Long-term growth rates are based on long-term

economic forecasts for growth in the manufacturing sector in the geographical

regions in which the cash generating unit operates. Pre-tax discount rates

specific to each cash generating unit are calculated by adjusting the Group

post-tax weighted average cost of capital (‘WACC’) of 9% for the tax rate

relevant to the jurisdiction before adding risk premia for the size of the unit,

the characteristics of the segment in which it resides, and the geographical

regions from which the cash flows are derived.

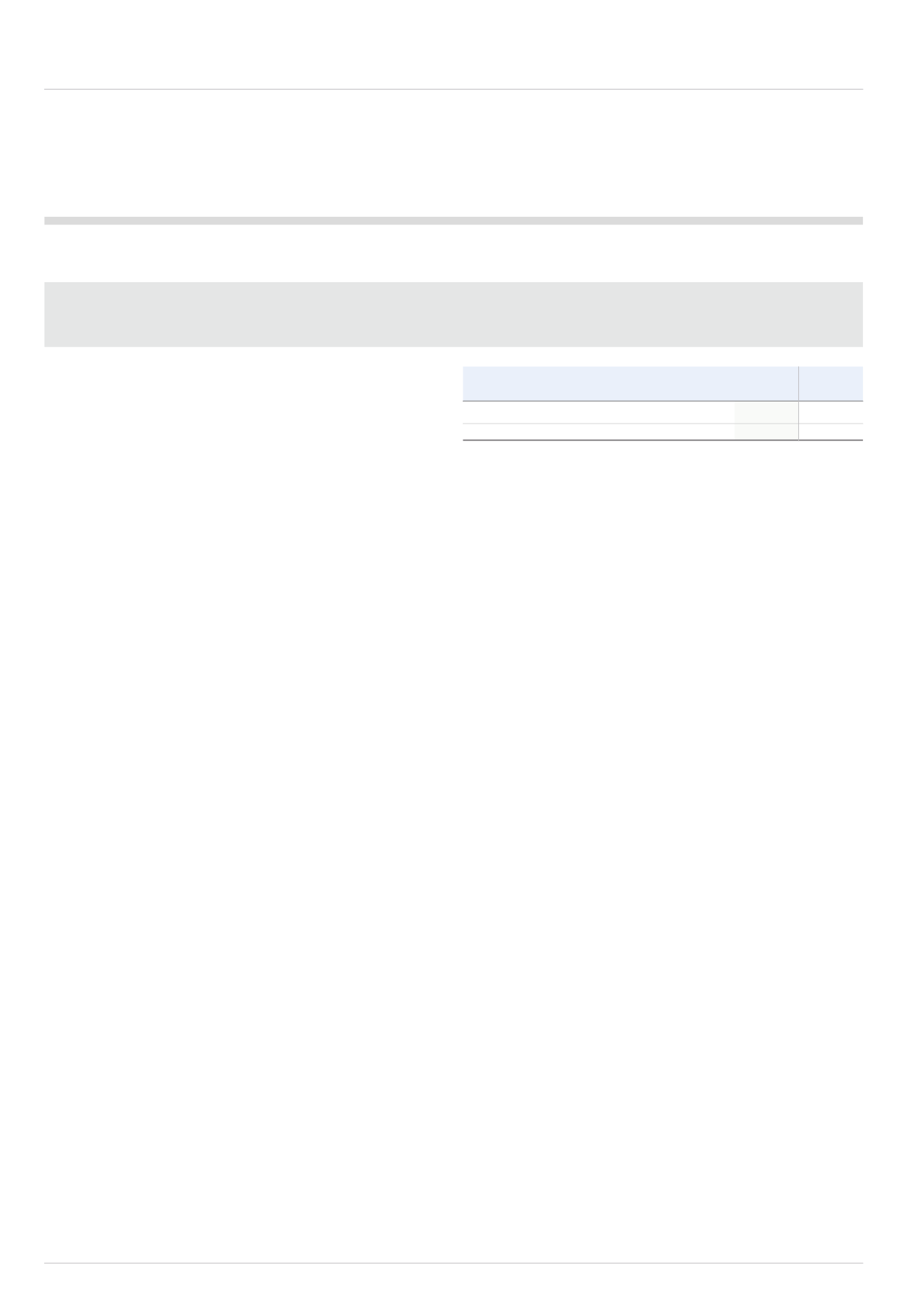

This exercise resulted in the use of the following ranges of values for the

key assumptions:

2014

2013

%

%

Pre-tax discount rate

9.8 - 16.4

10.6 - 14.6

Long-term growth rate

1.0 - 3.8

1.6 - 3.6

Following our impairment review, the goodwill associated with the Remosa

CGU, within the IMI Critical Engineering division was considered to be impaired.

This impairment has arisen due to a deterioration in the current trading base

of Remosa. A value in use calculation was used to determine the £48.4m

recoverable amount of the Remosa CGU, which used a discount rate of

13.8%. As a result the Group has recognised an exceptional impairment

loss of £26.9m.

As reported at the half-year and prior to disposal in October 2014, the Group

carried out a review of the recoverable amount of the AFP business due

to reduced expectations. This included a reassessment of the business’s

performance in the three to five years following the acquisition. This review

led to the recognition of an exceptional impairment loss of £10.8m, of which

£0.9m was against goodwill, partially offset by a deferred tax credit of £3.8m.

No amounts of goodwill that are significant in the context of the Group’s

total goodwill balance used the same key assumptions for the purposes of

impairment testing in either this year or the last. For the purpose of assessing

the significance in this context, the Group uses a threshold of 20% of the total

goodwill balance.

The aggregate amount of goodwill arising from acquisitions prior to 1 January

2004 which had been deducted from the profit and loss reserves and

incorporated into the IFRS transitional balance sheet as at 1 January 2004,

amounted to £364m. The cumulative impairment recognised in relation to

goodwill is £34m (2013: £6m).

The cumulative acquired intangible amortisation is £149.6m (2013: £136.0m).

SECTION 3 – OPERATING ASSETS AND LIABILITIES

Continued